1863 Power Of Attorney EMU (Early Matching Usage)… With A Twist!

In the section for “Power of Attorney, Voting” in Mike Mahler’s book U.S. Revenue-Stamped Documents of the Civil War Era, the first example he shows is a Voting Proxy from the Quincy Mining Company, the specific description and image as follows:

Quote:

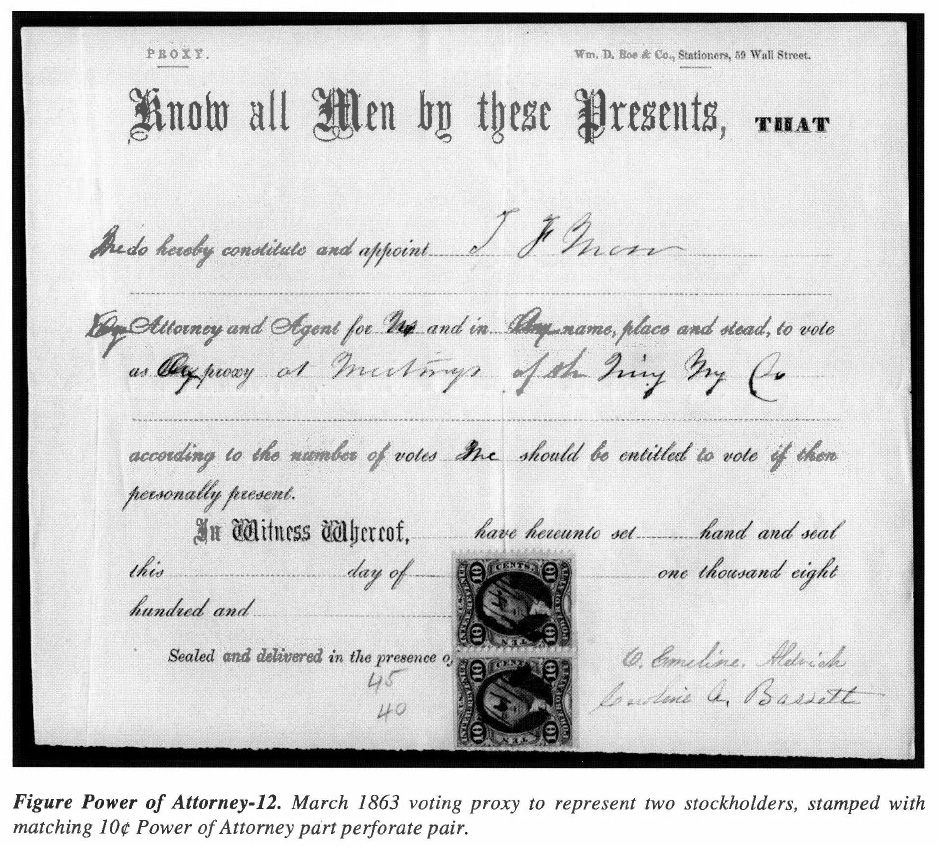

Form authorizing T.F. Mason to vote as proxy for Emeline Aldrich and Caroline Bassett at meetings of stockholders of the Quincy Mining Co., stamped with 10-cent Power of Attorney part perforate horizontal pair (perf between), manuscript cancel dated March 4, 1863, the form with New York imprint and probably executed there (Figure Power of Attorney-12). Opposite the women’s names are penciled “45” and “40”, presumably the numbers of shares they owned. It is not clear from the statute whether this document was to be considered two separate powers of attorney, or just one; in this case the former (and more expensive!) interpretation was made, but this was not always done (see Examples 4 and 6). It is known from other surviving Quincy Mining Co. documents that Thomas F. Mason was its President. I have recorded seven EMUs for this usage from the Quincy hoard (Mahler, 1996a), and more probably exist.

What ultimately prompted me to look this up was a similar piece that appeared on eBay, offered at auction but with a VERY high starting price, with Best Offer. What made it particularly interesting to me was that it has an illegal use of a 1-cent Franklin (Scott #63) along with a similar horizontally-oriented pair of R37b, dated February 27, 1863, a full week earlier than the Mahler example. However, 21 cents tax makes no sense, as the tax was $0.10.

Since the tax rate didn’t square up, I made a lowball offer of 70% below the starting price, which was autodeclined, so I back-burnered it. The more I thought about it though, it bothered me, as rate notwithstanding, the document fit my collection perfectly, being both an illegal usage and an EMU to boot.

I asked the seller whether there was any writing on the back of the document or any companion documents. I also mentioned the autodeclined offer. Unfortunately, there was no additional writing or companion documents, but after some back and forth discussion, the seller said they would consider my offer if the listing didn’t sell.

Two days later, even before the listing ended, the seller contacted me and said they had changed their autodecline settings and for me to make an offer. I guess there wasn’t any subsequent action on the listing. I resubmitted my original offer expecting a counteroffer, and lo and behold it was accepted.

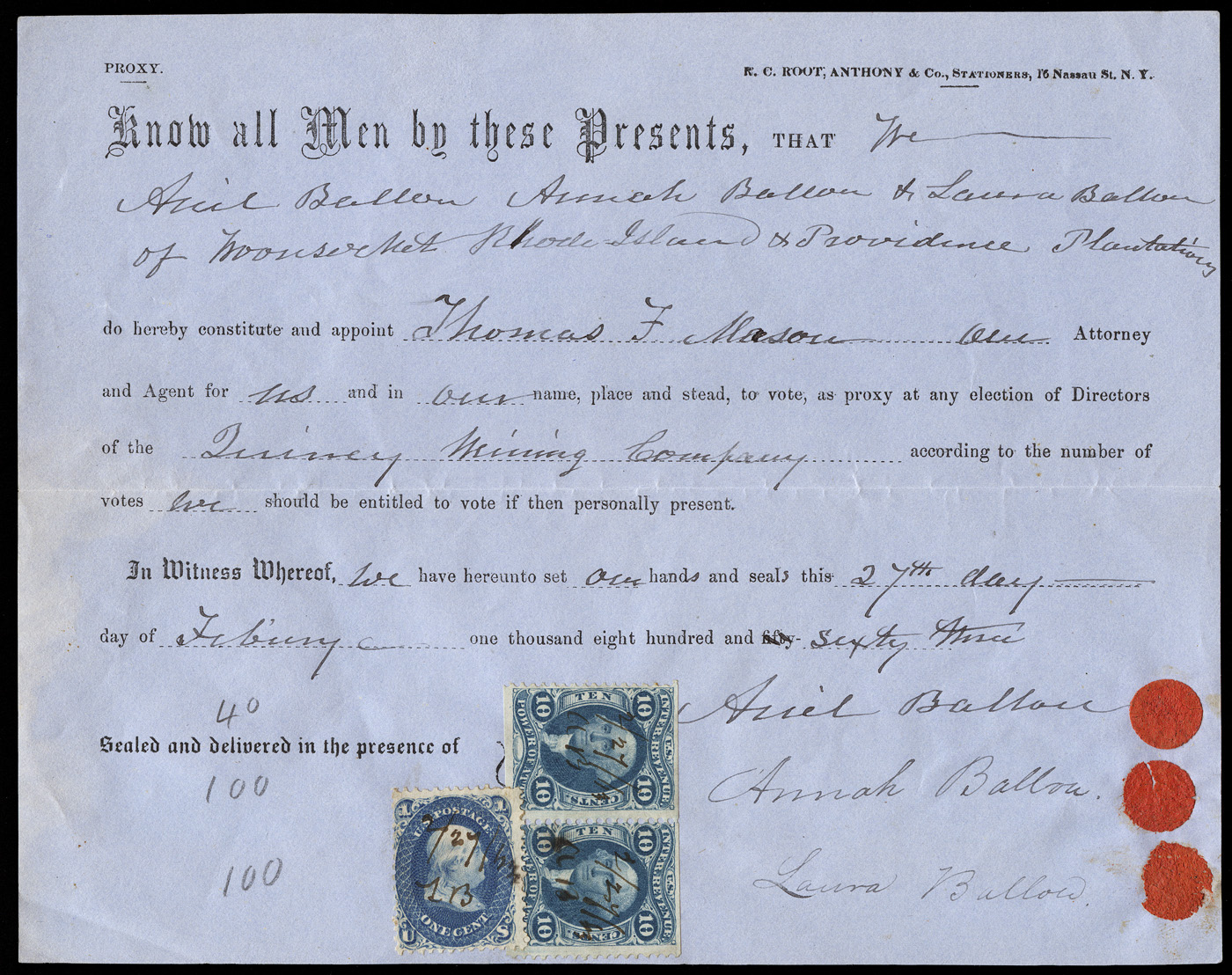

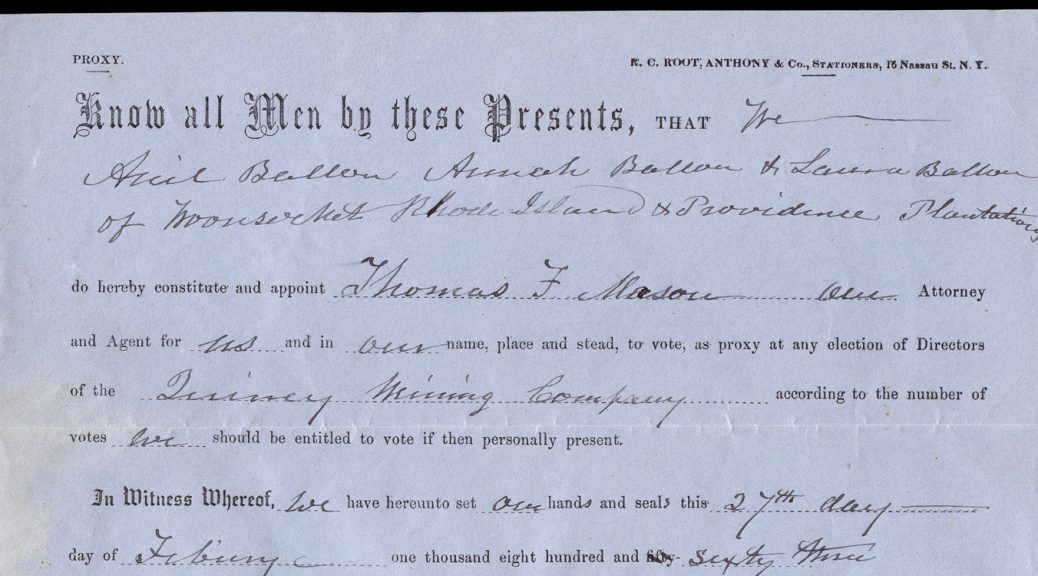

This proxy is for 3 (presumably) related parties: Ariel Ballow, Annah Ballow, and Laura Ballow. So using the same interpretation that Mike used, 10-cents per party would have been 30 cents tax. Either (1) when you’re in a hurry one blue stamp looks like another, or (2) they ran out of 10-cent Power of Attorney stamps and substituted something that looked close. There’s no reason to believe it’s contrived after the fact, as the hand matches on all of the cancels.

So this document was potentially doubly illegal: (1) using a postage stamp in lieu of a revenue stamp, and (2) short paying the tax due by 9 cents.

However the interpretation of 10 cents per shareholder vs. 10 cents per proxy document was apparently unclear at the time, as Mike mentions later in the section when referring to a similar proxy for the New York Central Railroad:

Quote:

…note that, as in Example 1, two distinct proxies were executed, but in this case only 10 cents tax was paid, and there is room for the interpretation that this was adequate. In 1867, however, it was ruled that on such documents 10 cents tax was required for each shareholder’s signature (Mahler, 1988d, 144).

So 30 cents tax due was correct and the document was doubly illegal after all.

A very nice addition to my illegal usage collection.